In Les Echos 10/11/2018

Make no mistake between a Russian gas delivery like Amazon and a US LNG delivery like Uber

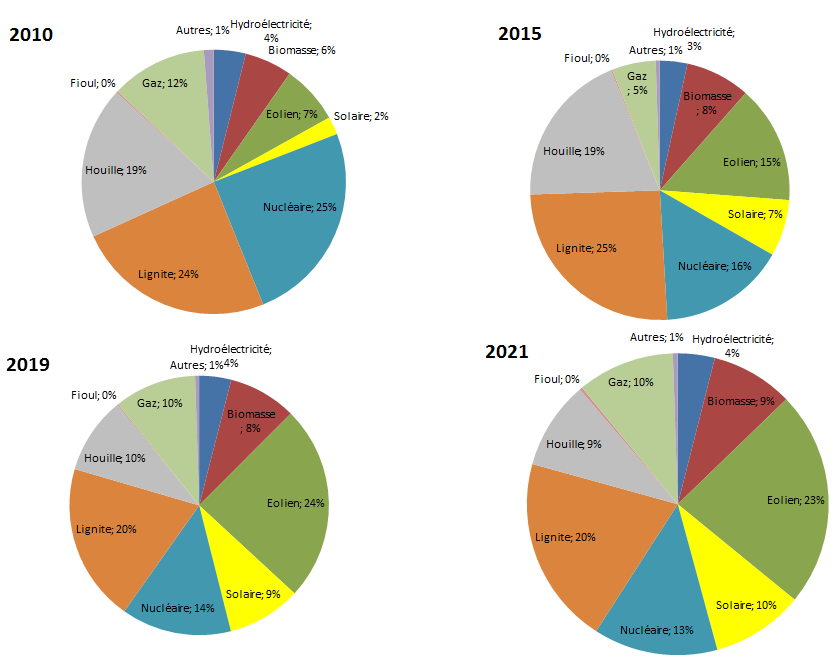

Since in the near future we will all be driving electric cars, our global problem is to eliminate the 40% of electricity produced from coal and lignite; and then to replace coal partly with natural gas. On our continent, mainly Northern and Eastern Europe are concerned: Poland 80% of electricity produced from coal, Germany 40%, Southern Europe and the Balkans between 25% and 40%, Ukraine 35%, Denmark 25%.

Two questions: how many m3 of gas will be needed to replace this coal and lignite? Who will supply this gas?

The world consumes nearly 4000 billion m3 of gas each year, 91% of which is transported by pipeline and 9% by LNG carrier. In 2017 the European Union consumed nearly 500Bm3. The supplying pipelines are already saturated, somes operate above nominal rates. Norway supplies 24%, Russia 35% and more than half of its gas passes through Ukraine. Algeria delivers the south. The Union imported about 49Bm3 of LNG in 2017. European domestic production is shrinking. In Groningen, it is also declining following earthquakes of January 2018. The Netherlands has become a net importer of gas.

Like every consumer of natural resources, Europe manages a Gas Consumer Doctrine that is expressed through influence strategies. On the other hand, the Gas Producer Doctrine of Russia, Algeria or Norway exercises a power. I have already explained these two concepts several times, especially here (enerpress). As long as everyone respects the terms of the contract, the producer delivers-the customer pays, this game works well. But it’s been disturbed for some time.

On the one hand, the United States has switched from a Gas Consumer Doctrine to a Shale Gas Producer Doctrine. Since US export LNG, their old slogan « Energy Independence » has changed to « Energy Dominance ». This commercial irruption is readable in a tweetered rhetoric: leadership, incitation, diplomatic pressure. It cuts Europe in two, as it tried to do in 1981 for another Russian gas story: the construction of the Fraternity gas pipeline.

On the other hand, Europe is also split in two because of Ukraine. The latter terminates its Russian gas transit and supply contract on 31 December 2019. Its network of gas pipelines, known as Fraternity, has been operating since 1984. It transports more than half of Russia’s gas to Western Europe. Transit brings in about $2 billion a year for Kiev, and its possible disappearance at the end of 2019 poses a budgetary problem. But Europeans also wonder about Fraternity. What is its actual maintenance, its actual operating capacity and life span? How long will it have a tangible capacity of 100 Mm3 per year according to the realists or 140 Mm3 according to Ukraine? Who does what and how, to renew or replace it and supply the Union?

For 50 years, Russia has been selling gas to European countries, particularly Austria. It has been supplying via Fraternity since 1984; since 2005, by the Yamal gas pipeline (33 Mm3) crossing Belarus and Poland; since 2011, by the Baltic Sea gas pipeline, Nord Stream1 (58 Mm3), directly to Germany without intermediaries. In the South, South Stream lands in Turkey and will one day end up in Bulgaria, Greece and southern Italy. In total, Russia will export to the Union in 2018 about 150Bm3, and Bm3 including Turkey, Belarus, Ukraine… In 2019, a new gas pipeline, twin to NS1, Nord Stream 2 (55 Mm3) will be operational. Finally, to address the Ukrainian issue, Germany has already offered compensation: the construction of a new Ukrainian gas pipeline with a capacity equal to Yamal with an exit point in Austria, but with a toll half as expensive as Fraternity.

Pending a constructive response to this last proposal, no one can reasonably oppose the construction of NS 2. Yet, guided in by a songe-creux Danish lobbyism, Poland and Ukraine are dragging their feet. The three of them are dangerously stirring up European nationalisms and hope to hinder the NS2 route by « bringing » Bornholm Island closer to the Danish coast. But no one is fooled. NS2 is already irreplaceable for European environmental safety! Indeed, if Germany stops its coal-fired electricity production by 2030, it would double its gas consumption, which in 2017 was around 132 Mm3. With its annual capacity of 55 Mm3, NS2 will allow Germany to make half of this anti-coal path (unless Fraternity becomes dangerously obsolete). The deal will also be economical; NS2 will deliver like NS1, in an Amazon’s way, directly to the customer without intermediaries.

For the other amount of gas needed to erase German coal, but also Danish, Polish, Ukrainian, Eastern and Southern European coal, LNG could be a solution. In the style of Uber, with an armada of LNG carriers, the United States can conquer this market through shale gas deliveries. In 2017, Europe has already bought 10% of the US LNG, compared to 5% in 2016; Poland supports this future strategy. It has signed two contracts with the US. These deliveries will start in 2019 and 2022. At least two other agreements will follow, as the objective is to deliver Ukraine via Poland and replace Russian gas.

This LNG solution should be considered with some caution, as the industry is still fragile. The 26 LNG terminals scattered throughout the Union are an asset. They will have a capacity of 218 Mm3 at the end of 2018, 40% of current European consumption. An additional 43 Mm3 will be added within 5 years. For example, Germany is considering an LNG terminal in Brunsbuettel. It will be able to receive 10% of the German gas from Algeria, Australia, Indonesia, Malaysia, Nigeria, Qatar, Russia, and the United States. However, European terminals were operating at only 27% of their capacity in 2017, and increasing this utilisation rate will be complicated for two reasons.

On the one hand, the number of gas loading terminals located in producing countries is unlikely to be sufficient by 2025 to provide a growing global demand, particularly in Asia (nationalism). For example, to supply Asia and Europe, the United States would only plan to have 85 Mm3 of LNG capacity in 2025, behind Qatar’s.

On the other hand, if nothing is done, the global LNG fleet, 467 ships in 2018, will remain undersized to meet the growing global demand for LNG, particularly in the Japan-Korea-China triangle. Reflecting this shortage, the spot price of this particular freight increased from almost $1,000 per day in 2016 to nearly $180,000 per day in 2018. Consequently, if the capacities of European terminals were to operate at 100%, nearly 2000 additional LNG tanker transits would have to be made to Northern and Southern Europe. They would use ocean routes sometimes overcrowded and therefore dangerous, such as the Channel and the Baltic Sea. Here, maritime oil pollutions linked to winter storms are bad memories. Finally, unlike a gas pipeline that does not pollute, LNG carriers pollute like a car running on LNG.

Final, for the time being, LNG has the fragility of a promising start-up, but the full consequences of its future cruising speed is not yet known. What would be the point if LNG could not be transported permanently but intermittently, neither in sufficient quantities nor in complete safety?

Europe’s gas future is evolving between the safety of a tube and that of an armada of LNG carriers. It is important to make no mistake between an Amazon gas delivery, in a pipeline, and an Uber gas delivery, in a boat. This strategic difference between Russian and American gas is also to be anticipated on the price of natural gas.

On average, the cost of producing Russian gas is close to $0.9 per million Btu and its transport by pipeline costs $1.2 MBtu to the Russian border. There, a 30% tax is levied, but it could be adjusted to keep the Russian gas price close to $2.5 MBtu. Gas resources enable Moscow to exercise a cost-volume strategy. These are the meanings of President Putin’s words when he talks about « economic decision » and not political decision.

The cost of producing U.S. shale gas is approximately $3-4 MBtu. Transportation costs are $2-3 MBtu. Total, $7 MBtu on average. However, commercial hegemony will require the United States to consider that the cost of extracting mixed shale oil and shale gas should be borne by oil alone. Thus, instead of being flared, shale gas would be exported with a break-even point at zero. Its selling price would just be equal to its transport cost. Without mentioning the word dumping, the United States would thus have shale gas deposits that would allow a focus strategy. This is the reason for President Trump’s anti-European trade anger.

In Northern Europe, prices are stable and close to $7 MBtu, while in the south they are higher between $7 and $10 MBtu between summer and winter. Spain has the largest number of LNG terminals. The United States insists that France pay for the Pyrenean interconnection. This is not a bad thing for balancing north-south prices downwards.

What should Europe do, where is its interest?

Europe’s interest is to reduce the cost of gas for its inhabitants. Its interest is therefore to promote the use of NS1 and Yamal, promote the construction of NS2, South Stream, or even the construction of a new gas pipeline to replace the Fraternity if it becomes obsolete. Its interest is also to promote greater use of its terminals and receive LNG from around the world, including the United States. It may also be necessary to build more terminals as European coal is erased. Finally, the Union’s interest is to promote the construction of LNG carriers, and probably to revisit their rules of navigation in its waters and straits.

It is also its interest to upset powerful strategies of producers via its influence strategies of consumer by achieving a major European crossroads of LNG-armed traders. Expanding this crossroads of European trading means increasing Europe’s North-South interconnections. Once the flagrant Franco-Spanish lock is opened, Algerian gas and LNG from the Persian Gulf via the under-employed Spanish terminals will move from South to North. Conversely, gas will move from north to south when LNG prices require rebalancing. Expanding the crossroads of European trading also means reaching the other south by improving the interconnections between Germany, Austria and France with Italy and Greece. Increasing the influence of trading in Europe and weakening supply in favor of demand means increasing LNG hybridizations, increasing the gas quantum dimension by multiplying European LNG capacities by 3, 5 or 10. Combating the fear of gas means continuing to reform the European gas market and turning it into blue gold

If it does this, Europe will eliminate the energy nationalisms emerging in Europe, it will also reduce the gas bill of Europeans, not by 30% as Poland indicated, but Brussels could halve the price of gas. Mechanically, the price of electricity will also fall.

What better way for us all to finally drive an electric car, without coal?