In Les Echos 04 10 2018

A few years ago, at the 10th anniversary of the Club de Nice, questions about the geopolitics of gas focused on the great global challenge of the time: Europe and Russia, who is dependent on whom? Was Europe dependent on Russia because of its 30% share of Russian gas imports, or was it Russia that was dependent on Europe because of its 80% share of gas exports to European consumers?

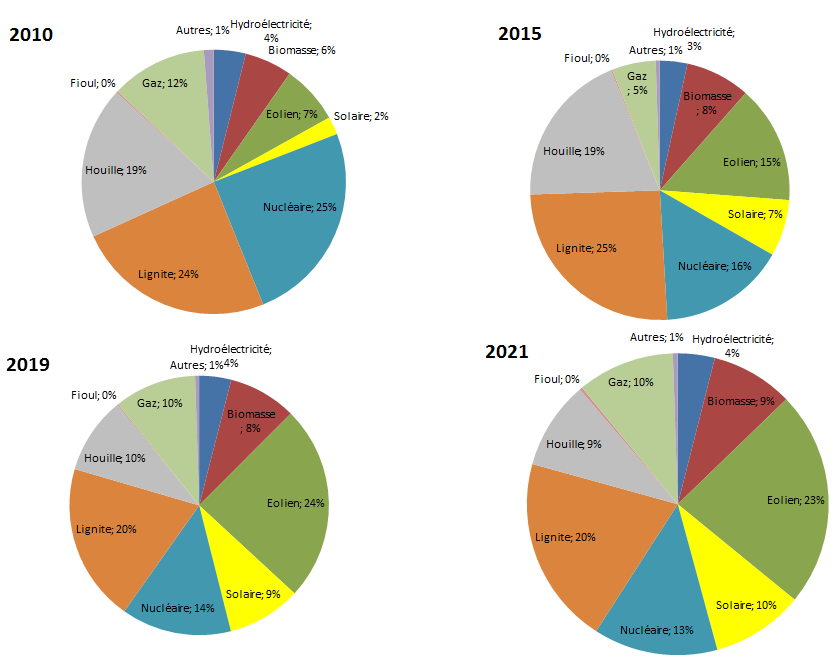

Since this binary challenge, the almost planned, determined and impermeable Russian-European bipolarity has become obsolete, giving way to a quantum dimension. The world of gas has changed: drop in production in Groningen and the North Sea; shale gas exploitation in the United States and soon in China; major replacement of coal by gas in the USA, Germany, Central Europe and China, which with 7% of world gas consumption becomes the 4th largest consumer worldwide behind the United States, Russia and Europe at 27; export of Russian, American, Australian, Qatari LNG to China and India; increase in Japanese imports due to temporary nuclear shutdown; diversification of oil price signals to spot prices, etc.

These intertwined gas events each have their own but uncertain logic. Its decoding depends on the changing nature of observers. The fertility of the unexpected far exceeds our imaginations; it is the new quantum geopolitics of gas.

Deus ex machina of this gas anti-determinism, LNG currently represents only 10% of global gas consumption. However, its future role will be immense. Indeed, when the consumer is more than 4000 km from the producer, the cost of LNG is higher than that of the pipeline. But this kilometric breakeven drops…

In terms of LNG production, in a few years’ time, the top four (Qatar, Australia, the United States and Russia) will be followed by Africa, Canada and Southeast Asia.

On the consumption side, Japan, still the world’s largest LNG consumer, is being caught up by China as it « de-carbonises », while South Korea’s imports, equal to those of Europe, will remain stable as long as it does not contribute to the renovation of Pyongyang’s energy mix. By 2030, this Asia (Japan, Korea, China, excluding India and Southeast Asia) will consume nearly 100% more LNG than in 2018; 55% of this consumption will be Chinese instead of 25% in 2018. Beijing will import from Australia 45%, Qatar 11%, Russia 7%, Malaysia 7%, then Indonesia, PNG, United States, Canada, etc.

Given the volumes, the Chinese issue seems disproportionately more complex than the European one. However, unlike China, it is not yet possible in Europe to rely on indigenous unconventional gas exploitation. And, since Germany and Italy are the first customers there (England « brexited » will play alone), in northern Europe the Nord Stream 1 submarine pipeline, which has been in operation since 2011-2012, will be doubled by Nord Stream 2 and will supply Germany and France directly; the south will be supplied by the “Nabucco-South Stream-Turkish Stream” pipeline (we do not know how to name it anymore). In the centre, the Yamal onshore gas pipeline supplies Austria and eastern Germany.

While these four pipelines increase European supply by about 20% compared to the flow of the old Brotherhood Soviet onshore pipeline (which pays the famous transit fee to Ukraine), gas géopolitologues are frightened.

Is the fear economic? Would the bypassing of Ukraine by gas pipelines in the north and south send Brotherhood back to waste? It could be answered that the use of coal in Germany and Eastern Europe must decrease in favor of gas, and from this point of view the volumes of Brotherhood will remain indispensable.

Is the fear political? Will the two gas export flows cut off European customers in two: one in Western Europe and the other in the east? Will Russia play two different European gas diplomacy, particularly with regard to Ukraine? A customer is no longer a good customer if he doesn’t pay. Therefore, when the Berlin Wall collapsed, just as Europe and the United States would never have promised not to extend NATO to Russia’s markets, Russia would never have promised not to focus on Ukraine. In the game of bluff, Russian roulette has consequences other than those of poker.

For 50 years the fear of Russian gas has been a classic. Disguised as an individual or collective unconscious, it permeates the geopolitical imagination. However, the importance of gas revenues is so crucial for the Russian State that contractual disruptions are prohibited. In other words, for the European countries that pay their gas bills, how many times have Russian gas deliveries failed in 50 years?

In any case, as long as no nonsense such as a « metals war » is written about a « gas war », uniting with the risks of gas pipelines, make divorce possible.

Both Beijing and Brussels are gas hubs. Beijing is sourcing from the Pacific, Gulf and Siberia. Europe, with five Russian gas pipelines facing it, also supplies itself from the Mediterranean, the Gulf and the United States.

Upsetting potential power strategies of producers via influence strategies of consumers, will be achieved through a major European crossroads of LNG-armed traders and a temperate substitution of the dollar by the euro. Expanding this crossroads of European trading means increasing Europe’s North-South interconnections. Once the flagrant Franco-Spanish lock is opened, Algerian gas and LNG from the Persian Gulf via the under-employed Spanish terminals will move from South to North. Conversely, gas will move from north to south when LNG prices require rebalancing. Expanding the crossroads of European trading also means reaching the other south by improving the interconnections between Germany, Austria and France with Italy and Greece. Increasing the influence of trading in Europe and weakening supply in favor of demand means increasing LNG hybridizations, increasing the gas quantum dimension by multiplying European LNG capacities by 3, 5 or 10.

Combating the fear of gas means continuing to reform the European gas market and turning it into blue gold.