In La Tribune 23/12/2019

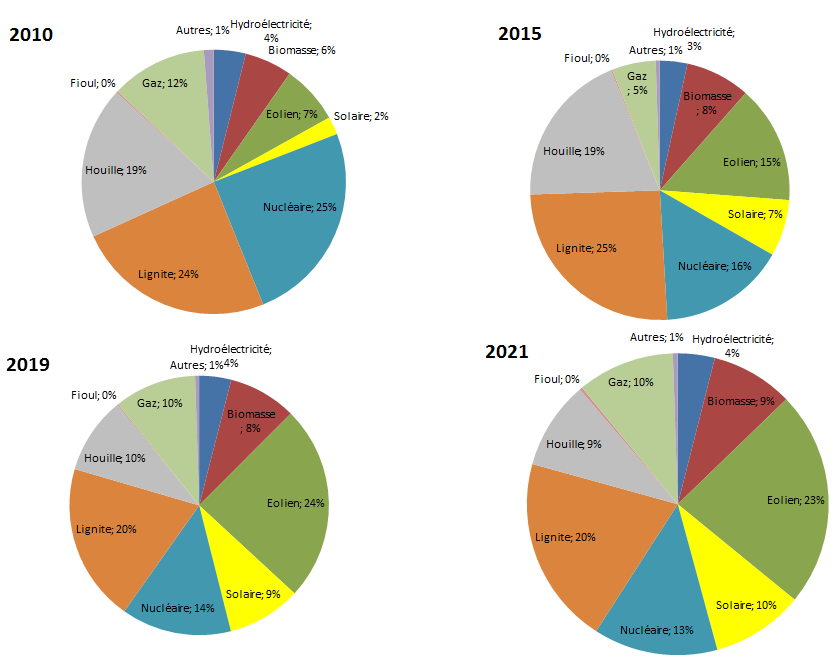

By abandoning coal and lignite, Germany, Poland and Eastern Europe will return to a state of high electricity dependency when renewable energies are insufficient. Supporting the opposite is a fake-news as corrosive as the striped record of the « rare metals » hoax (see video).

At a time when we must protect ourselves from the climate curse, only natural gas can ensure the substitution of coal at a low cost. But its European production is in free fall. It was around 270 Bm3 five years ago, it will only be around 200 Bm3 in five years’ time: the Netherlands became a net importer and production in Norway and the United Kingdom is stable at 175 Mm3.

Conversely, demand for natural gas is increasing. The 550 Bm3 that will be consumed by Europe in 2020 (14% of world demand), will be burned 75% in industry and households and 25% in power generation. As a result, Europe’s gas dependency is already vast, 350 Bm3 per year, and it will increase further as coal and lignite generators are replaced by gas. The European dilemma is clear: where will gas come from?

Putin and Trump’s Christmas present

Russia already covers about 62% of our dependence on gas pipelines. Operating above nominal rates, they saturated in 2019 after transporting 210 Bm3. They will be slightly relieved in 2020 thanks to the 55 Mm3 of the Nord Stream 2 subsea pipeline, the sister pipe to Nord Stream 1, which will enable Germany to double its direct gas supply capacity from Russia, 110 Bm3, without the Ukrainian and Polish transits of the two pipelines Fraternity and Yamal. However, it will need to acquire other sources to replace its lignite by 2038.

It is therefore almost contradictory in the midst of the Donbass conflict and yet fortunate that this week Moscow and Kiev signed the agreement allowing the continued delivery of gas to Europe via Ukraine. This is Putin’s Christmas present to Europe, together with a cheque for USD 2.9 billion for Kiev.

In response to this agreement, the US energy power strategy sanctioned the European companies financing Nord Stream 2. This punishment is Trump’s Christmas present. Less pleasant than Putin’s, it is the fruit of Talion diplomacy and nevertheless indicates that Washington wants to sell its gas to Europe as much as Moscow does. Its main ally is Poland. Viscerally opposed to Nord Stream 2, it will serve as a bridgehead for the LNG of American shale imported into its ports by boat. It will consume it and dump it in Ukraine in order to compete with gas from Moscow, drive down prices, and even later oppose the renewal of Russian gas transit to Western Europe.

This Polish-Ukrainian perspective does not bother about the future risks of a drop in gas exports from Washington, which are nevertheless possible for two reasons.

Firstly, if Trump is not re-elected in 2020, Democrats Warren and Sanders are considering increasing technical restrictions on the hydraulic fracturing needed to produce oil and shale gas, as well as prohibiting oil companies from accessing federal lands that account for 20% of current production. Will this risk of a drop in production from 2021 be weakened by the impeachment attempt initiated by the Democrats, which paradoxically could increase Trump’s chances of re-election?

Secondly, a large debt weighs on 45% of US production in the hands of small producers ruined by low gas prices. They can go bankrupt and cause a world-class price mess. As part of President Trump’s energy domination strategy, will the oil majors be commandeered to take over their operations and ensure the continuum of production and exports to Europe?

Benefits of the new « brexited » United Kingdom

This situation has been discussed at length here: the schism between Russian gas in Western Europe and US LNG in Eastern Europe, nationalism and peace, energy independence or domination. The recent and very significant Russian gas victories clarify the rules of the game in the East, while in the West, US shale LNG will see the uncertainty lifted after the result of the presidential election next November.

Moreover, since the pivot of these European negotiations is in Poland, it is worth noting that the latter’s infatuation with Washington is likely to find a new ally in the United Kingdom « brexited ». These two countries will have to defend in gas and other areas common visions and interests different from those of Brussels.

Let’s conclude this brief geopolitical energy review with an optimistic outlook. Our continent shares its long-term energy risk between three suppliers: Russia, US shale LNG and Middle Eastern and African LNG for Southern Europe. Each is forced to follow a prisoner’s strategy to retain or gain market share.

A harbinger of this future favourable gas profusion, while the average European gas price over the last 7 years at the TTF spot is above 19 €/MWh, is the current price, in winter, at around 14 €/MWh. If well managed, future competition for the European market could ensure a projection of an attractive long-term average price of between €9 and €14/MWh.